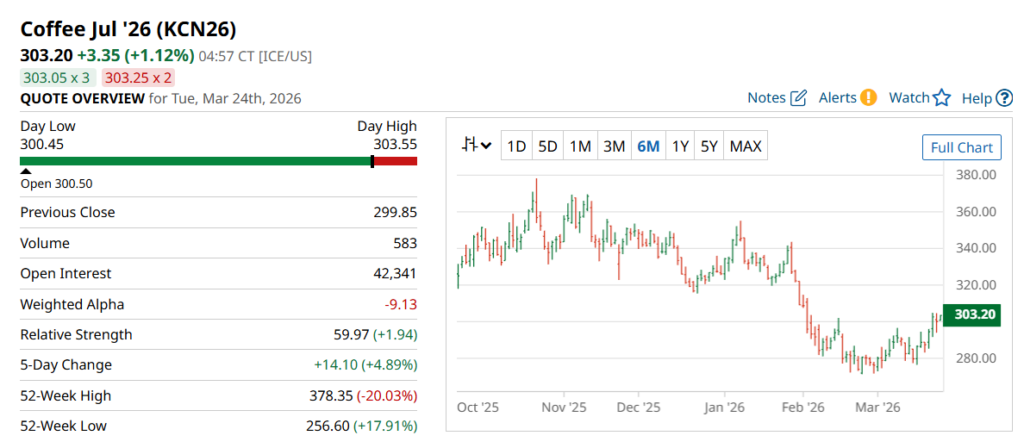

Source: Barchart (Coffee Jul ’26 Futures – KCN26)

As of March 24, 2026, Coffee C Futures are trading at approximately 303.20 US cents/lb.

Over the past six months, the market has moved through three distinct phases:

- Peak: ~370–380 cents/lb

- Correction: ~270–280 cents/lb (~25–30% decline)

- Recovery: Stabilizing above 300 cents/lb (~10–12% rebound)

This price behavior indicates volatility followed by consolidation, not structural weakness.

The key level to monitor is 300 cents/lb. Holding above this range signals that global Arabica demand remains intact despite short-term corrections.

For exporters and buyers, this benchmark is not theoretical. It directly influences Indonesian Arabica coffee prices, particularly for export-grade green coffee beans.

The current condition is clear:

- The market has corrected from its peak

- It has found support above 300

- It is now stabilizing within a high-price environment

This sets the foundation for understanding why Indonesian prices have adjusted locally—without indicating a broader market decline.

Indonesian Arabica Coffee Prices (March 2026)

Current Indonesian Arabica coffee prices (export grade Double Picked) are trading in the range of:

- IDR 150,000 – 165,000 per kg

Compared to the previous month:

- IDR 170,000 – 175,000 per kg

Month-on-month change:

- Down approximately 8–12%

This correction is consistent across major producing regions:

- Sumatra (Aceh, North Sumatra — including Gayo)

- Java

- Sulawesi

- Flores

While Gayo is often used as a reference in the export market, the current price movement is not origin-specific. It reflects a national-level adjustment across the Indonesian Arabica supply.

Price Context

Despite the decline, current price levels remain structurally elevated when viewed against historical norms.

This indicates:

- The market is cooling from a recent peak, but is not entering a downturn

- Export pricing is adjusting to short-term supply pressure, not weakening demand

Export Market Behavior

At current levels:

- Exporters are actively moving fresh harvest volume into the market

- Price reductions are measured, not aggressive discounting

- Most sellers are aligning with global benchmarks rather than undercutting

This is a critical distinction.

The market is not reacting to panic or oversupply.

It is adjusting to increased availability during harvest flow, while maintaining alignment with the global price structure.

This establishes the baseline for Indonesian Arabica:

lower than last month, but still within a strong pricing cycle.

Indonesian Robusta Coffee Prices

Current Indonesian Robusta coffee prices (Grade 1, export grade) are in the range of:

- IDR 70,000 – 80,000 per kg

- Market average: approximately IDR 75,000/kg

Market Structure

The price relationship between Arabica and Robusta remains consistent:

- Arabica ≈ 2× Robusta

This spread is stable and reflects:

- Quality differentiation

- Processing standards

- End-market demand (specialty vs commercial use)

Stability vs Arabica Volatility

Unlike Arabica, Robusta has not experienced a meaningful correction.

Current conditions show:

- Stable supply flow

- Consistent buyer demand

- Minimal speculative pressure

There is no indication of:

- Oversupply

- Aggressive price movement

- Structural imbalance

Market Behavior

At the exporter level:

- Robusta is trading on steady contract flow, not opportunistic buying

- Buyers are continuing regular procurement cycles

- Pricing remains anchored and predictable

This makes Robusta less reactive to short-term shifts compared to Arabica, which is more exposed to global futures volatility.

Position in the Current Market

Robusta is currently acting as a stability anchor within the Indonesian coffee market:

- No sharp correction

- No rapid upward movement

- Consistent transactional activity

This reinforces the broader structure:

- Arabica = volatile but high-value

- Robusta = stable and volume-driven

Why Indonesian Coffee Prices Declined

The recent decline in Indonesian Arabica prices is driven by seasonal supply dynamics and short-term buyer behavior, not structural weakness.

Three primary factors explain the adjustment:

1. Early Harvest Flow Increasing Supply

Indonesia is entering the early phase of its harvest cycle.

Typical harvest structure:

- Sumatra (Aceh, North Sumatra): April–June (earliest flow)

- Java, Bali, Sulawesi: May–August

- Flores: Later in the cycle

Peak harvest (“panen raya”) generally occurs between July and September.

Current Market Impact

As of March–April:

- Early harvest from Sumatra begins entering the market

- Fresh crop availability starts to increase

- Exporters prepare for larger inflow in the coming months

At this stage:

- Supply pressure is emerging, not at peak levels

- Exporters begin positioning for volume movement, not scarcity

This early increase in availability is sufficient to soften prices, especially after a high-price period.

2. Slower Buyer Activity After Late-2025 Buying

Following aggressive purchasing in late 2025:

- Importers are currently holding inventory

- New contracts are more selective and delayed

- Buyers are waiting for a clearer direction during harvest progression

Impact:

- Reduced transaction frequency

- Lower short-term upward pressure on price

This is a timing adjustment, not a demand collapse.

3. Local Market Adjustment vs Global Stability

Despite global Coffee C futures holding above 300 cents/lb, Indonesian prices corrected due to local factors:

- IDR/USD exchange rate movement

- Existing forward export commitments

- Anticipation of a larger supply during peak harvest (Q3)

A weaker rupiah allows exporters to remain competitive in USD terms, while local prices adjust downward in IDR.

Result:

Indonesian prices can decline ahead of peak harvest, even when global benchmarks remain stable.

Summary of the Decline

The current price movement reflects:

- Early-stage harvest supply entering the market

- Buyers are delaying purchases ahead of the larger upcoming supply

- Currency and local market adjustments

This is a pre-peak harvest correction, not a signal of weakening global demand.

Market Interpretation: Correction Within a Strong Cycle

The current price movement should be read in context.

Indonesian Arabica prices have declined, but the underlying structure of the market remains intact.

What the Market Is Signaling

- Global Arabica benchmark remains above 300 cents/lb

- Price decline in Indonesia is limited to ~8–12%

- Supply increase is seasonal and expected

This combination indicates:

- No structural demand weakness

- No market breakdown

- No forced liquidation or distress selling

Instead, the market is undergoing a controlled adjustment driven by timing.

Key Distinction: Local Correction vs Global Strength

There is a divergence between:

- Global pricing (stable, elevated)

- Local Indonesian pricing (temporarily softer)

This divergence is driven by:

- Early harvest flow entering the market

- Buyer hesitation ahead of peak harvest (Q3)

- Currency and local supply chain dynamics

This is a normal pattern in origin markets.

What This Means in Practice

- Prices are adjusting to increased availability, not falling demand

- Exporters are still pricing in line with global benchmarks

- The broader market remains structurally supported

In practical terms:

The market is not weakening.

It is recalibrating ahead of peak harvest supply.

Position of the Current Market Cycle

The current phase can be defined as:

- Post-peak correction

- Pre-peak harvest positioning

- Stabilization within a high-price environment

This is typically a transitional window, not a long-term trend reversal.

Buyer Positioning: Short-Term Entry Window

Current conditions present a tactical entry window for buyers.

Indonesian prices have corrected due to early harvest flow, while global benchmarks remain structurally strong. This creates a temporary gap between local pricing softness and global market support.

What Buyers Are Seeing Now

- Lower entry prices compared to February 2026

- Increasing availability from early harvest (Sumatra flow)

- Continued support from Coffee C above 300 cents/lb

At the same time:

- Sellers are active, not holding aggressively

- Supply is building, but has not yet peaked

- Competition among buyers is currently reduced

Where the Risk Lies

This window is not open-ended.

As the market moves toward peak harvest (July–September):

- Buying activity is likely to resume

- Export allocations will begin to tighten

- Strong global benchmarks will reassert upward pressure

Buyers delaying purchases are effectively assuming:

- Continued weak demand

- Sustained oversupply

- Further price downside

At this stage, those assumptions are not supported by current market signals.

Strategic Positioning

The current environment favors:

- Securing volume during early harvest flow

- Locking in prices before broader market re-entry

- Taking advantage of temporary supply-driven softness

This is not a distressed market.

It is a controlled correction within an elevated pricing cycle, creating a short-term opportunity rather than a long-term decline.

Short-Term Price Outlook (Indonesia)

Expected near-term pricing range:

- Arabica: IDR 150,000 – 170,000 per kg

- Robusta: IDR 70,000 – 80,000 per kg

Likely Market Direction

In the short term, the market is expected to move:

- Sideways, as early harvest supply continues to enter

- With upward pressure, if buying activity resumes or supply tightens

Key variables to monitor:

- Progression toward peak harvest (July–September)

- Changes in importer purchasing activity

- Movement in Coffee C futures above or below 300 cents/lb

- IDR/USD exchange rate, affecting export competitiveness

Market Bias

- Downside risk is limited by strong global benchmarks

- Upside risk increases as:

- Harvest flow stabilizes

- Buyer activity returns

- Export inventories tighten

This creates an asymmetric setup:

- Limited short-term downside

- Gradual upward pressure over time

Bottom Line

- Global Arabica remains strong, holding above 300 cents/lb

- Indonesian prices corrected due to early-stage harvest supply

- Buyer activity is temporarily slower, not structurally weak

The current market reflects a pre-peak harvest adjustment, not a decline cycle.

This creates a short-term buying opportunity within a structurally strong market.

Get Current Indonesian Coffee Prices & Availability

Export pricing and stock levels are dynamic and origin-specific.

For:

- Latest Indonesian coffee price list (Arabica & Robusta)

- Available volumes by origin (Sumatra, Java, Sulawesi, Flores)

- Current export schedules and shipment options

→ Contact us directly or request the latest wholesale pricing.