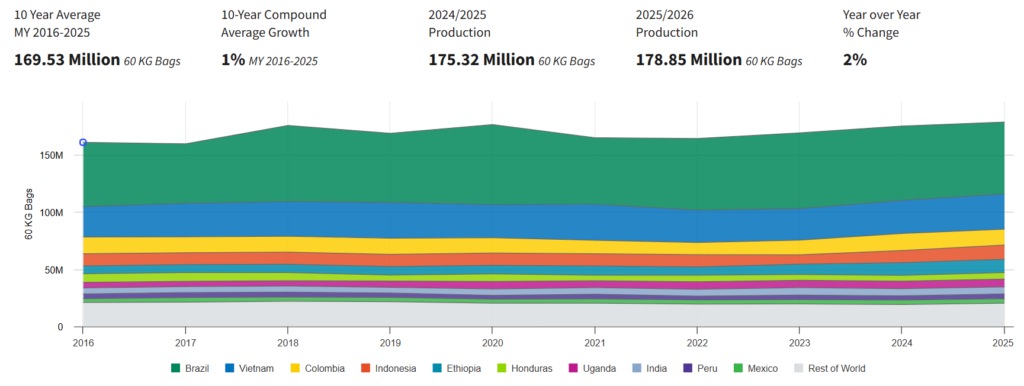

Global coffee production continues to expand, but at a structurally slow pace. In the 2025/2026 marketing year, total output is projected to reach 178.85 million 60-kg bags, reflecting a modest 2% year-over-year increase. Over a longer horizon, the industry shows even more limited momentum, with a 10-year compound annual growth rate of just 1% (2016–2025).

This slow growth is a critical signal. While global demand for coffee, driven by emerging markets, specialty consumption, and café culture, continues to rise, production is not scaling at the same rate. The result is a tightening balance between supply and demand, which directly influences price volatility and sourcing strategies.

At a structural level, the coffee industry is not experiencing rapid expansion like other agricultural commodities. Instead, it is constrained by factors such as climate variability, aging plantations, limited land expansion, and labor challenges in producing countries. These constraints mean that even small disruptions in key origins can have disproportionate effects on global supply.

Within this context, understanding the role of major producing countries becomes essential. Supply is highly concentrated, and shifts in a handful of origins, particularly Brazil, Vietnam, and Indonesia, can reshape the global market. For buyers and importers, this makes origin-level analysis not optional, but necessary for long-term sourcing decisions.

Disclaimer: All data presented in this analysis is compiled from publicly available sources, primarily the USDA Foreign Agricultural Service (FAS) database: https://www.fas.usda.gov/data/production/0711100.

Global Coffee Production Breakdown: Who Controls Supply

Global coffee production is highly concentrated, with a small group of countries accounting for the majority of the supply. This concentration creates structural dependency in the market; any disruption in these key origins has immediate global consequences.

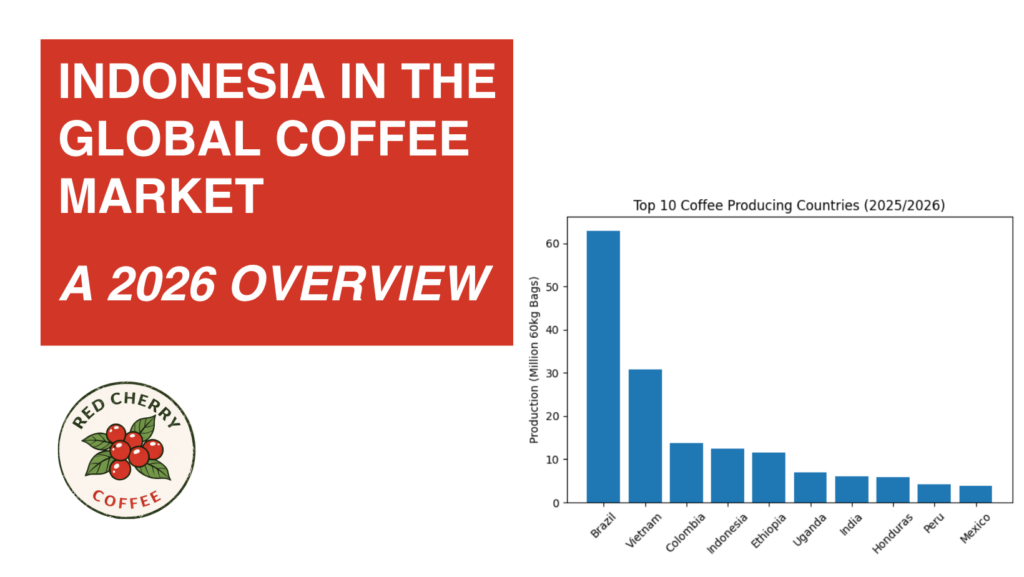

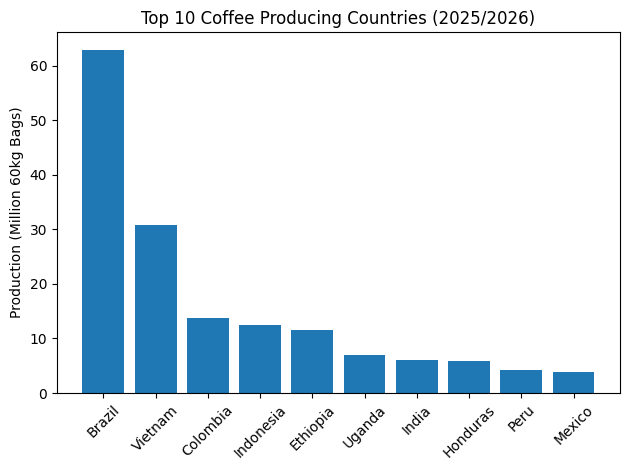

Based on 2025/2026 projections, the distribution of production is as follows:

- Brazil — 35% (63 million bags)

- Vietnam — 17% (30.8 million bags)

- Colombia — 8% (13.8 million bags)

- Indonesia — 7% (12.45 million bags)

- Ethiopia — 6% (11.56 million bags)

- Others (Uganda, India, Honduras, Peru, Mexico) — smaller but relevant shares

Brazil alone produces more than one-third of the world’s coffee, making it the single most influential player in determining global supply levels and price direction. Vietnam, heavily focused on Robusta, dominates the commercial and instant coffee segment, reinforcing its role as a volume-driven supplier.

Indonesia, at 7% of global production, ranks among the top four producers worldwide. This position is often underestimated. While Indonesia does not match Brazil or Vietnam in scale, it plays a critical role in diversifying global supply, particularly in both Robusta and specialty Arabica segments.

However, the structure of Indonesia’s coffee sector differs significantly from its competitors. Unlike Brazil’s highly industrialized production or Vietnam’s efficiency-driven output, Indonesia’s supply is more fragmented, with a large portion coming from smallholder farmers. This results in:

- Less consistency in volume year-to-year

- Greater variability in quality across regions

- Higher reliance on intermediaries within the supply chain

From a buyer’s perspective, this creates a trade-off. Indonesia offers distinct flavor profiles and origin diversity that are difficult to replicate elsewhere, but it requires more deliberate sourcing strategies to ensure consistency and reliability.

The implication is straightforward: global coffee supply is not evenly distributed, and Indonesia’s role—while smaller in volume—is strategically important. Buyers who understand how to navigate this structure gain access to differentiated products that are less exposed to the commoditized segments dominated by Brazil and Vietnam.

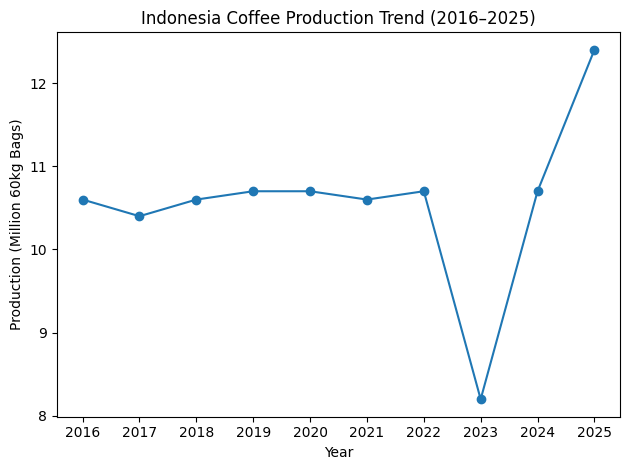

Indonesia’s Coffee Production Trend (2016–2025): Stable, but Not Scaling

Indonesia’s position as a top global producer is established, but its growth trajectory tells a different story. Unlike Brazil or Vietnam, which have shown clearer scaling patterns, Indonesia’s production over the past decade is largely flat with periods of volatility.

Between 2016 and 2025, Indonesia’s output has fluctuated within a relatively narrow range of ~10 to 12.4 million 60-kg bags. There is no consistent upward trend—only short-term movements driven by seasonal and structural factors.

Key Observations from the Data

- 2016–2020: Stable baseline around 10.4–10.7 million bags

- 2021–2022: Slight stagnation, no meaningful growth

- 2023: Significant drop to 8.2 million bags

- 2024–2025: Recovery phase, reaching 12.4 million bags

This pattern indicates that Indonesia is not operating in a growth cycle, but rather in a recovery-and-fluctuation cycle.

What’s Driving This Volatility

Several structural constraints explain this inconsistency:

- Climate sensitivity → rainfall variability directly impacts yield

- Smallholder dominance → limited standardization and scalability

- Aging trees → reduced productivity without systematic replanting

- Fragmented supply chain → inefficiencies from farm to export

These are not short-term issues. There are structural limitations that prevent Indonesia from scaling production at the same pace as more industrialized producers.

Implications for Buyers and Importers

From a sourcing perspective, Indonesia presents a different risk profile compared to Brazil or Vietnam:

- Supply is available, but not always predictable

- Volume consistency requires active supplier management

- Quality can vary significantly between regions and harvest cycles

However, this volatility also creates a strategic advantage. Because Indonesia is less industrialized, it retains origin diversity and unique cup profiles that are increasingly valuable in the specialty market.

Key Takeaway

Indonesia is not a high-growth producer; it is a strategically important but structurally constrained origin.

For buyers, this means one thing:

You cannot approach Indonesia with a commodity mindset. You need a sourcing strategy.

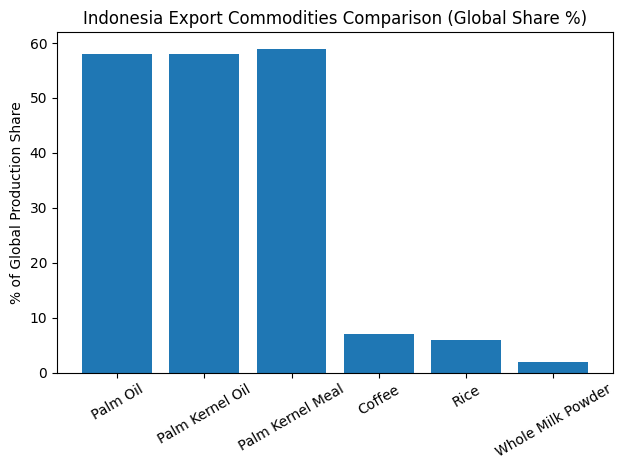

Indonesia’s Coffee in the Context of Its Broader Export Economy

To understand Indonesia’s coffee sector accurately, it must be viewed within the country’s wider agricultural export structure. Coffee is globally significant, but domestically, it is not a dominant commodity.

Compared to other Indonesian exports, coffee operates on a smaller scale:

- Palm oil accounts for approximately 58% of the global production share from Indonesia

- Palm kernel derivatives also exceed 50% global share

- Rice and other staples maintain strong domestic and regional importance

- Coffee, by contrast, represents only ~7% of the global production share

This contrast is critical. While Indonesia is a top-four global coffee producer, it does not prioritize coffee at the same level as palm-based commodities. The difference is not just in volume, it is in industrial focus, investment, and infrastructure.

What This Means Structurally

Because coffee is not the primary export driver, the sector evolves differently:

- Lower industrialization compared to palm oil

- Less centralized supply chains

- Limited large-scale investment in productivity improvements

- Greater reliance on traditional farming systems

This explains why Indonesia’s coffee production remains relatively flat over time, while other commodities scale more aggressively.

Hidden Advantage: Why This Still Matters

At a surface level, this lack of industrial focus appears to be a disadvantage. But from a market perspective—especially in specialty coffee, it creates a unique positioning.

Because the sector is less standardized, Indonesia retains:

- High regional diversity (Gayo, Java, Toraja, Flores, etc.)

- Distinct processing methods (wet-hulled, natural, honey)

- Flavor profiles that are difficult to replicate at scale

In contrast, highly industrialized producers tend to prioritize consistency over uniqueness.

Implications for Buyers

For international buyers, this creates a clear distinction:

- If your priority is volume efficiency and price stability, markets like Brazil and Vietnam dominate

- If your priority is origin differentiation and specialty value, Indonesia becomes strategically important

However, this advantage only materializes if sourcing is managed correctly. Without proper supplier relationships and quality control, the same structural fragmentation that creates uniqueness can also introduce inconsistency.

Key Takeaway

Indonesia’s coffee sector is not built for scale; it is built for diversity and differentiation.

For buyers, the implication is direct:

Indonesia should not be approached as a bulk commodity origin, but as a strategic source of unique and high-value coffee.

Market Implications: What This Means for Coffee Buyers

The data presented is not just descriptive; it has direct implications for how coffee should be sourced, priced, and positioned. Most buyers make the mistake of treating all origins under the same procurement logic. That approach fails in Indonesia.

1. Supply Growth Is Structurally Limited

Over the past decade, global coffee production has increased from approximately 155–160 million bags to around 170–175 million bags, implying a compound annual growth rate of roughly ~1%. However, this growth is not linear and is characterized by significant year-to-year volatility driven by major producing countries. This creates a baseline condition:

- Tighter supply cycles

- Higher sensitivity to disruptions

- Increased price volatility

Indonesia amplifies this dynamic. Because its production is not scaling consistently, it cannot act as a stabilizing supplier in the same way Brazil often does.

Implication:

Buyers relying on spot purchasing or short-term contracts are exposed to supply risk.

2. Indonesia Is Stable—But Not Predictable

Indonesia consistently produces coffee, but not with precision. The fluctuation from 8.2M (2023) to 12.4M (2025) is not a minor variation; it is a structural signal.

This means:

- Availability can shift significantly within short periods

- Harvest outcomes directly affect export volume

- Supplier reliability varies widely depending on network strength

Implication:

Consistency is not guaranteed by the origin—it is created by the supplier.

3. Commodity Strategy Will Fail in Indonesia

If you approach Indonesia the same way you approach Brazil or Vietnam—focused purely on:

- Price per metric ton

- Volume efficiency

- Standardized specs

You will encounter:

- Inconsistent quality

- Supply gaps

- Operational friction

Indonesia’s structure does not support a purely commodity-driven model.

Implication:

You need a sourcing strategy, not just a purchasing process.

4. Where the Real Opportunity Lies

Indonesia’s weakness in industrial scale is exactly where its strength emerges.

Because the sector is:

- Less standardized

- Less optimized for bulk output

- More regionally diverse

It produces coffees that are:

- Distinct in flavor profile

- Less interchangeable with other origins

- More valuable in specialty and differentiated markets

This is where margins are created, not in bulk Robusta trading, but in origin-driven positioning.

5. Strategic Positioning for Buyers

There are only two rational ways to approach Indonesia:

Option 1 — Volume Buyer (Commodity Focus)

- Use Indonesia as a supplementary origin

- Accept variability

- Prioritize blended usage

Option 2 — Strategic Buyer (Value Focus)

- Build direct supplier relationships

- Focus on specific regions (Gayo, Java, Toraja, etc.)

- Leverage uniqueness for product differentiation

Most buyers attempt a hybrid approach and fail—because they expect consistency while refusing to invest in a sourcing structure.

Key Conclusion

Indonesia is not a plug-and-play origin.

It rewards structured sourcing and penalizes transactional buying.

For buyers who understand this, Indonesia offers access to highly differentiated coffee with long-term strategic value.

For those who do not, it becomes a source of inconsistency and operational risk.

Conclusion: Indonesia’s Role in a Constrained Global Coffee Market

The global coffee market is not entering a phase of rapid expansion. With production growth limited to ~1% annually, supply will remain structurally tight relative to demand. In this environment, the importance of origin strategy increases, not decreases.

Indonesia sits in a distinct position within this system.

It is:

- A top-four global producer

- A non-scaling but resilient origin

- A diverse and under-industrialized supply base

These characteristics define both its limitations and its value.

On one side, Indonesia cannot compete with Brazil or Vietnam in terms of:

- Volume consistency

- Industrial efficiency

- Price stability

On the other hand, it offers what those markets cannot:

- Origin diversity

- Unique processing methods

- Non-commoditized flavor profiles

This creates a clear divide in how Indonesia should be approached.

Buyers looking for interchangeable, volume-driven supply will find more predictable options elsewhere. But buyers focused on product differentiation, specialty positioning, and long-term sourcing strategy will find Indonesia increasingly relevant.

The key variable is not the origin itself—but how it is sourced.

Final Strategic Insight

The global coffee market is moving toward:

- Greater demand for differentiation

- Increased pressure on supply

- Higher expectations for traceability and consistency

Indonesia aligns with this shift—but only for buyers who approach it correctly.

The advantage is not in buying Indonesian coffee.

The advantage is in knowing how to source it.

Next Step

If you are evaluating Indonesian coffee for your supply chain, the priority should not be price alone. It should be:

- Supplier reliability

- Origin clarity

- Long-term consistency

These factors determine whether Indonesia becomes a competitive advantage or a sourcing liability.

Work With a Reliable Indonesian Coffee Partner

Sourcing Indonesian coffee is not just about finding availability; it is about ensuring consistency, clarity, and long-term reliability in a structurally complex market.

For buyers who want to move beyond transactional purchasing, working with the right partner becomes a critical factor. A structured sourcing approach can reduce variability, improve quality control, and provide better visibility across origin, processing, and logistics.

At this stage, the question is not whether Indonesia offers value; it clearly does. The question is whether your current sourcing model is equipped to capture it.

If you are:

- Experiencing inconsistency in supply or quality

- Looking to secure stable access to Indonesian coffee

- Exploring specialty origins such as Gayo, Java, or Toraja

- Or planning to build a more reliable sourcing pipeline

Then it is worth initiating a direct conversation.

Redcherry.coffee works with international buyers to streamline Indonesian coffee sourcing, focusing on origin transparency, supplier coordination, and consistent export quality.

You can explore available products or submit an inquiry directly by clicking the contact button below:

A structured sourcing relationship is not an upgrade; it is a requirement in markets like Indonesia.